;

![]()

Non-Performing Exposures - CEE

Disposal / Acquisition strategy – key legal considerations

Preface

Throughout the CEE/SEE region, the gross NPE ratio has more than halved from its peak of 9.8 % in the first half of 2014 (when we published the second edition of this guide) to 3.8 % at the end of 2019. From 2014 to 2019, NPE volumes decreased from EUR 65.7bln to EUR 33.8bln (see source).

However, the COVID-19 pandemic has put new pressure on global as well as CEE/SEE economies.

Many regulators and legislators have swiftly reacted to the pandemic, for example by introducing moratoria. Also, many states have introduced state-supported financing/guarantee schemes to fuel their economies.

While the scope of these measures (moratoria as well as state-supported financing) varies from jurisdiction to jurisdiction, they have one factor in common: they are temporary and will expire at some point in time (soon). And while the magnitude of the spike in non-performing exposures and its timing is still uncertain, many are expecting a cliff-edge effect when these measures expire.

In combination with a hugely compressed interest rate environment that adversely affects banks' ability to generate earnings (required to counterbalance the impact of increased provisioning on banks' balance sheets), this is likely to lead to another surge in transactions in non-performing exposures (portfolios as well as single-name corporate exposures).

Also, the development of efficient secondary markets for distressed assets is one of the key pillars of the NPLs strategy presented by the European Commission on 16 December 2020.

We therefore take great pleasure in presenting to you the third edition of our thoughts on some key legal issues which sell- and buy-side industry participants should consider when examining the viability of NPE transactions (single names and portfolios) in the CEE/SEE region. We seek to combine this with observations about legal and market (standard) practice developments that have taken place since the last edition of this guide.

Pick and choose your countries: Please select the countries you wish to see the answers for:

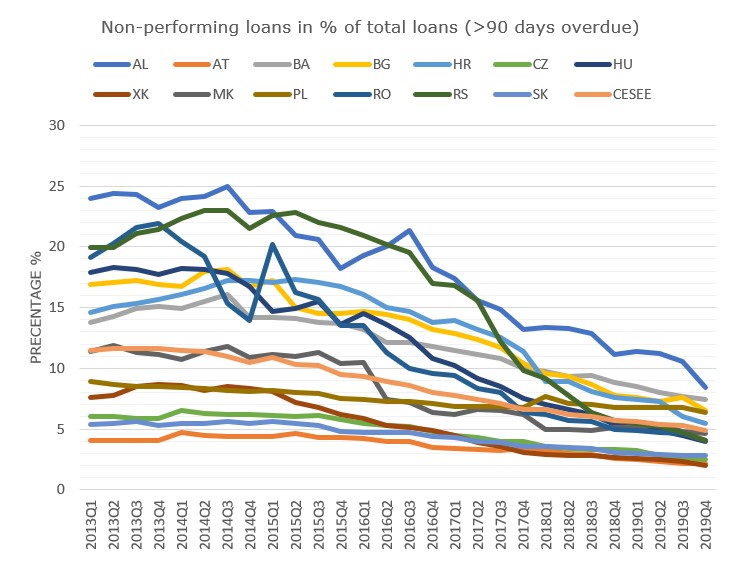

Since its peak in 2013/14, the relation of non-performing loans to total bank loans (expressed in %) has steadily declined, as shown in the following graph:

[click to enlarge the graph]

(CESEE Bank Lending Survey Spring 2020 (EIB), Facts on Austria and Its Banks (OeNB))

From the authors' perspective at the time of writing, it is difficult to predict the exact magnitude of the economic effects of the COVID-19 pandemic. However, legislators, regulators and banks appear to accept as a likely scenario that high volumes of new non-performing exposures (NPEs) inflows will emerge once the economic effects of the crisis begin to materialise.

Since March 2020, European lawmakers, regulators and policymakers have reacted swiftly in their attempts to alleviate the impact of the COVID-19 pandemic on banks' balance sheets.

- Measures relevant in the present context of non-performing exposures focus on introducing flexibility to the rules on forbearance as well as accounting rules, notably IFRS 9. Statements on using flexibility within accounting and prudential rules were made by the Basel Committee of Banking Supervision, the European Banking Authority (EBA) and the European Central Bank, amongst others. The EBA guidelines of 2 April 2020 specifically deal with public and private moratoria on loan repayments.

- On 28 April 2020, the European Commission adopted a comprehensive banking package aimed at facilitating bank lending to support the economy and help mitigate the economic impact of the pandemic. The package proposes a few targeted "quick fix" amendments to the EU's banking prudential rules (the Capital Requirements Regulation) in order to maximise the ability of banks to lend and absorb losses related to COVID-19. The Interpretative Communication on the EU's accounting and prudential frameworks that is part of the banking package confirms the statements on using flexibility within accounting and prudential rules (see above).

- Further targeted efforts in the context of non-performing loans include proposed amendments to the securitisation framework set out in the Securitisation Regulation (EU) 2017/2402 that were published on 24 July 2020. If implemented, the proposed amendments will remove some regulatory obstacles to the securitisation of non-performing exposures.

- At the time of writing, the EBA has – after initially signalling a phase-out of the regulatory "leeway" embodied in its Guidelines on legislative and non-legislative payment moratoria as of September 2020 – re-activated these until 31 March 2021, in anticipation of a larger-than-expected increase in NPEs.

- Last but not least, on 16 December 2020, the European Commission published its NPLs strategy in response to the COVID-19 pandemic. The development of efficient secondary markets for distressed assets is one of the key pillars of that strategy.

How banks will react to the anticipated increase of NPEs remains to be seen. Judging from a recent uptick in transactional activity (where some smaller portfolios have been sold, arguably as "test-balloons") we would conclude that disposals of distressed and non-performing exposures are high in demand when it comes to banks' strategies for managing their NPEs. This would also be consistent with developments in CEE, where as a corollary to the number and volume of transactions which have taken place over the past years we have observed notable positive developments in terms of the reliability, speed and quality of deal-making in the NPE market.

As in any other transaction, legal and regulatory issues are only some of the aspects that impact the success or failure of structuring, implementing and executing a buy- or sell-side NPE transaction. Other key driving factors include the economics of the deal, accounting, tax, reputational and general risk management considerations. But in our experience, legal considerations (including in relation to servicing and enforcement) are among the key drivers when it comes to selling or buying a portfolio or single tickets of distressed exposures. This is not only due to the nature of the parties involved, in particular regulated sell-side and partly regulated buy-side businesses, but mainly due to the nature of the assets involved in the transaction, whether a single-name loan claim or a portfolio of (consumer) credit claims.

Below we have set out our thoughts on how to strategically approach a sell or buy-side NPE transaction. Many of the issues addressed will be equally relevant to portfolio as well as single-name (corporate exposures) transactions.

This guide is structured according to transaction stages, from pre-transaction decision-making, through structuring aspects and transaction execution, to post-execution servicing.

2.1 Pre-transaction aspects (decision-making)

A potential sell-side credit institution has many options for managing its clients in distress, ranging from restructuring the debt to forcing borrowers into liquidation.

When considering whether the disposal of certain assets or asset classes may be an optimal strategy for actively managing distressed credits, the management of the potential sell-side institution will have to carefully consider whether the perceived negative effects are outweighed by the advantages.

On the down side, there may be negative effects on an institution's financials, because of losses realised on a sale of assets that are not marked-to-market in an institution's books or because of an unfavourable tax treatment. This might be combined with the threat of foregoing the upside that may potentially come from a successful recovery or even from enforcement. In addition, institutions may be concerned about managing reputational aspects – and the potentially resulting increased scrutiny by consumer protection authorities and/or legal challenges/claims proceedings. That said, we have observed that since the previous (2014) edition of this publication NPE transactions have become a regular feature and are attracting significantly less controversy with the stakeholders.

On the other hand, the most obvious benefit of a successfully completed sale of NPEs is the effect on NPE ratios and risk-weighted assets (RWAs) and the resultant freeing up of equity and, depending on provisioning levels, even immediate P&L effects. Selling institutions, who courtesy of EBA's 2018 Guidelines on disclosure of non-performing and forborne exposures are compelled to make enhanced disclosures in relation to NPEs, have also received positive market and shareholder feedback. This includes rising stock prices once a transaction or series of transactions has been announced and completed, as well as a positive ratings response to the improvement/enhancement of remaining on-balance sheet assets in connection with a perceived increase in focus on that institution's core activities (originating new business) while "outsourcing" certain aspects of problem loan management. Finally, the removal of NPEs from a bank's balance sheet will result in a notable reduction of the administrative burden associated with carrying NPEs, not least in the form of the various reporting and disclosure requirements, as set forth, for example, in the aforementioned EBA Guidelines.

2.1.1 Challenge yourself (sell-side)

- Do I have the organisational and managerial capacities to manage and service distressed exposures in a value-preserving manner and at least in the same quality as experienced third-party special servicers?

- What will be the likely effect on my financials of selling non-performing exposures (substantially) below par?

- Is the jurisdiction of my target portfolio accustomed to NPE transactions or should I be wary of negative stakeholder reception risks (such as increased scrutiny by regulators and/or a "wave" of legal challenges / claim proceedings by debtors)? What mitigants can I put in place to address such risks?

- Am I able to define a portfolio that suits expectations on data quality, credit quality, maturity and pricing?

2.2 Structuring aspects

Once an institution concludes that disposals of single names or portfolios of non-performing exposures form an important pillar of its overall strategy of actively managing its problematic exposures, it is time to decide on the overall transaction structure (auction process, directly negotiated sales, etc.) and to start the vendor due diligence process that precedes most successful sale transactions.

Accurate, reliable and complete data about the non-performing exposures are the key to maximising sales proceeds. It is often at this stage of preparing information for potential investors when institutions learn more than they expected about their own customers/borrowers and the quality and consistency of documentation and data available in relation to the distressed credits.

In addition to practical aspects in relation to the completeness of documentation and data quality, one has to consider that any sell-side (credit) institution will normally be bound by data protection (GDPR), banking secrecy and – depending on the identity of the envisaged investors – competition laws. These rules limit or even prevent the full disclosure of data (including commercially sensitive data) to potential buy-side institutions and their advisors. However, that dilemma can usually be overcome in a manner that satisfies compliance considerations as well as investor due diligence requests. The available options range from disclosure of anonymised/pseudonymised and aggregated data only, to full disclosure of the credit documentation to due diligence advisors formally appointed/endorsed by the selling institution. Those advisors would in turn produce a report to the potential investor on an aggregated and no-name basis only (i.e. without referencing specific loans and customers).

In certain jurisdictions, the aforementioned measures are, as a matter of practice, often coupled with a (seller's) requirement that the purchasing entity meets certain criteria in order to be eligible to acquire an NPE portfolio. For example, the use of buy-side securitisation special-purpose entity may reduce the risk of falling foul of certain secrecy requirements.

By the same token, during this pre-sale vendor due diligence process, sell-side institutions are well advised to scrutinise the credit files relating to the portfolio to be sold to determine whether they contain only the information and data necessary/required by a potential buyer for enforcement purposes. This is because disclosure would typically have to meet an interest balancing test and, likewise, be limited to a strictly "need-to-know basis" (interpretations of this latter requirement vary across jurisdictions).

A fully fledged buy-side due diligence of each credit file has proven to be disproportionally costly (despite support from AI). In certain jurisdictions it could even potentially run afoul of limitations on information disclosure and data transfer. Therefore, selling institutions have in recent years often considered (usually with the assistance of financial and legal advisors) only disclosing samples of, say, 5 % to 10 % of all loan contracts relative to transactions included in the portfolio. This was done on the basis that this constitutes a representative sample of documentation used, including that there are no significant deviations in documentation standard. Consequently, buy-side due diligence was, in certain transactions, limited to the loan contracts included in this sample. Nevertheless, we have observed in practice that selling institutions, especially in non-retail NPE portfolios, have rather tended to lean towards "fuller" disclosure. This is driven, on the one hand, by the fact that material corporate exposures by their nature require more in-depth disclosure, both to support the sell-side pricing estimations and to meet the due diligence requirements of investors. More generally, this was in response to investors' demand for increased contractual protection (in terms of amplified representations/warranties and remedies) in regard to assets where the underlying documentation was not made part of the disclosure package.

Finally, structuring considerations will come into play during this phase of a transaction. In addition to tax (particularly VAT and withholding tax considerations as well as limitations on deductibility of losses resulting from the transfer), the structure will largely be driven by the legal aspects of the transferability of loans and related security interests. Outright assignment is by and large the most preferred and common transfer mechanism, used in instances where title to target assets can be passed to the purchaser without debtor consent, cumbersome/costly re-registration procedures or similar hurdles. In terms of alternatives for tackling transferability hurdles, synthetic structures (trusts or sub-participations, typically on the basis that "elevation" into an outright assignment will occur upon overcoming a particular hurdle) and corporate transactions (spin-off/hive-down) have, in the past, often been successfully deployed in CEE/SEE NPE practice.

2.2.1 Challenge yourself (sell-side)

- Have I used consistent documentation when originating the loans subject to the transaction?

- Are all required customer consents or alternative legal grounds (e.g. based on balancing of interests as recognised by the GDPR and some banking laws) for data processing and information disclosure available?

- What are my alternative options (in the relevant jurisdiction) for transferring and disclosing data and information in a compliant way during due diligence stages and afterwards?

- Am I legally required / practically in a position to strip-off non-core information from the credit files so that disclosure can be limited to data and information on a need-to-know (least intrusive) basis?

- Are the loan receivables and related security interests transferable (under the terms of the contracts and applicable law(s)) or do I need to explore a synthetic (trust or sub-participation) or corporate transaction (such as a spin-off/de-merger of the portfolio)?

Buy-side institutions, on the other hand, when gearing up to participate in a sales/auction process, will be keen to validate their pricing and valuation models against the local legal environment (e.g. their assumptions in terms of collection and enforcement as well as insolvency proceedings). Moreover, they will be looking into setting up a legally compliant and tax-efficient acquisition structure, where their focus will be on compliance with local banking (licensing), consumer protection and servicing regulation. Not least, they will be looking into how the acquisition will be financed.

2.2.2 Challenge yourself (buy-side)

- Do I have the requisite local experience to adequately price the NPE portfolio or is additional due diligence on the local legal and tax regimes required?

- Will the structure I usually use be feasible in the local environment? In particular, will the acquisition vehicle or the servicing vehicle (if different) have to be licensed?

- Is professional servicing expertise available locally or do I have to build this and at what cost?

2.3 Transaction execution

Sell-side institutions will usually be looking at a two-stage sales process, which would commence by asking interested bidders for indicative bids based on a standard information package or fact book made available by the seller.

After this pre-selection process, shortlisted bidders would normally be granted access to additional information to allow them to complete their due diligence and to submit binding bids. The contents and level of detail of the data room / data tape and related access rights will be driven by competition law considerations as well as banking secrecy and data protection laws (see above) and, at times, also by operational and timing constraints.

In a well-structured process, at this stage the proposed transfer and (transitional) servicing documentation would be made available by the sell-side institution to shortlisted bidders. Documentation will largely be driven by issues relating to the transferability of loan receivables and related security, where parties aim at achieving a transfer without debtor involvement. Also, implementing an appropriate allocation of risks (representations/warranties and remedies) and a suitable transfer of servicing of the target portfolio post-closing are key (also see below). As mentioned above, transferability aspects will be decisive in establishing whether an outright assignment of the assets can be implemented or whether the portfolio will have to be transferred synthetically or even hived off from the selling institution's balance sheet into an SPV by means of a corporate transaction with a subsequent sale of that SPV's shares to the investor. This may have a material impact on the overall transaction calendar.

Irrespective of whether the parties pursue an asset or share deal transaction, any buyer will be well advised to not only focus on the desired receivables and security interests transfer, but to also verify whether the structure chosen may have undesirable effects. Such effects could for example arise from creditor liability and/or employee transfers (such as being treated under local laws as a transfer of a business unit). Legal diligence will be required to explore how these risks can best be mitigated. We may observe that, as a matter of practice, the market standard seems to be moving towards a solution whereby such risks are removed from the transaction perimeter by means of indemnities or equivalent buyer protections stipulated in the sale and purchase documentation.

Similarly, the seller will also have to consider continued implications in terms of legal/contractual obligations and liability also after the implementation of the envisaged transfer. For example, assignments of loan receivables are typically not designed to impact/transfer "historic" creditor liability for the time period between origination and up to and including the agreed cut-off date for economic transfer. Therefore, the seller may continue to be bound by information obligations as well as "historic" creditor liabilities/obligations toward the assigned debtors/consumers.

In addition to the receivables transfer documentation, agreements governing the (transitional) servicing and enforcement of the exposures sold and purchased will normally have to be put in place. Whether the servicing will be performed by third-party servicers or by the selling institution on behalf of and for the account of the purchaser will, in addition to banking secrecy and data protection considerations, be determined on the one hand by the servicing capabilities of local special servicers and the selling institution. On the other hand, regulatory and reputational risk considerations of the selling institution in relation to servicing on behalf of, and at the instruction of, the investor will be relevant.

Other ancillary documents may include a data trust agreement if the involvement of a data trustee is required from a banking secrecy or data protection perspective, also in regard to non-performing exposures, and financing documentation at the buyer's end.

2.3.1 Challenge yourself (buy-side)

- Does the transfer documentation result in legally robust transfer/establishment of rights (in respect of the loan receivables, related security and other ancillary rights) required to effectively manage the target portfolio?

- Will the proposed transfer mechanism require the involvement of debtors or trigger costly and/or cumbersome notifications, re-registrations of collaterals or recommencement of enforcement action (potentially coupled with the risk of time-barring)?

- Is there a risk that the transfer will also trigger the assumption of ("historic" / consumer protection or other) liabilities and/or employees attached to the loan portfolio by the buyer? How can this be avoided / mitigated (also in terms of risk allocation provisions in the transfer documentation)?

- Does local law allow a timely transfer of enough data to the purchaser and the servicer to allow a seamless continuance of servicing/enforcement?

2.4 Post-execution servicing

Once the data needed by the servicer to perform its duties is legitimately available to it, the transaction will enter the key value driving stage. The buyer's return will depend primarily on the results yielded by the servicer when servicing the portfolio and when enforcing the loan receivables and related security as well as on the time needed to recover the non-performing receivables.

At this stage debtors will often attempt to raise various types of defences, both in relation to the underlying credit and security documentation as well as in relation to the validity of the transfer to the buyer. The buyer will therefore have to concern itself to provide evidence of transfer to local courts and enforcement authorities in compliance with local laws.

2.4.1 Challenge yourself (buy-side)

- Does the servicer hold all licences required under local laws to perform its duties?

- Has the buyer (or a data trustee) / servicer obtained the documentation required to service the loan portfolio (credit files) in a legally compliant manner?

- Has the buyer obtained all means of evidence required under local laws to prove the validity of the transfer of receivables, related security and other ancillary rights to local courts?

austria

The limitations resulting from secrecy obligations (data protection and banking secrecy, the latter of which is enshrined in Austrian constitutional law) at due diligence stages are often addressed by appropriate precautions to avoid customer-specific disclosure to investors. This proves exceedingly difficult for large corporate exposures and in a single-name context, where, on the other hand, the courts' scrutiny of data disclosure consents is less stringent than in a consumer context.

Until late 2012 the general view, which was also confirmed by the Supreme Court with respect to a subrogation structure, was that secrecy obligations should not bar a credit institution from selling and assigning loans, since particularly in respect of non-performing loans, the interests of the bank outweigh the customers' legitimate interests in keeping their data secret. In this context, two Supreme Court judgments, in which the Supreme Court held that an assignment of receivables in violation of Austrian banking secrecy is null and void, took some industry participants by surprise.

While structuring a transaction this risk is usually addressed by using purchasing vehicles that by law are subject to banking secrecy (as is the case for qualifying securitisation SPVs) and that will obtain information and data subject to secrecy only upon consummation (closing) of the transaction. During due diligence stages, customary structures – that admittedly can be cumbersome and costly – seek to avoid direct bidder access to data but rather try to extend banking secrecy to involved (due diligence) advisors.

Finally, the assignment of receivables and other rights may be subject to Austrian stamp duty, if a deed is set up evidencing the transaction. However, certain transactions are exempt, including the assignment of receivables between credit institutions, assignments to securitisation SPVs, and assignments under a factoring contract. In addition, certain strategies are used in order not to trigger Austrian stamp duty (e.g. by avoiding an Austrian nexus).

bosnia & herzegovina

Each of the two self-governed entities, the Federation of Bosnia and Herzegovina and Republika Srpska, has a separate legal system. While the laws applicable to NPL transactions are to a large extent harmonised, parties may still encounter different obstacles depending on where the transaction takes place. In this overview we focus on challenges common to both legal regimes.

During deal structuring foreign exchange regulations that prohibit a cross-border sale and assignment of loan receivables will have to be considered carefully. Accordingly, a foreign purchaser needs to set up a local acquisition company in order to acquire local customer receivables.

From a licensing perspective, retail loan receivables can be transferred only to a licensed entity, i.e. a bank or a licensed financial organisation, while purchasing of corporate loan receivables is not subject to bank licensing.

The parties will also have to consider limitations in relation to banking secrecy and data protection, which are either novel or not tested before the courts of Bosnia and Herzegovina and which, if not addressed adequately during structuring stages, could result in a true impediment to the effective transfer and assignment of receivables, ancillary rights and related security.

For true sale, NPE receivables and ancillary rights are usually transferred by assignment agreement. To the extent the transaction involves secured loan receivables, however, the transfer of related security (mortgages, pledges, etc.), while presumed to be assigned together with the receivable as an accessory right, will be perfected only upon re-registration with the competent register. In practice this can result in a costly and time-consuming process. In addition, while consents of debtors under the transferred loan are not required, they need to be notified of the assignment.

bulgaria

Under Bulgarian law, data protection and banking secrecy limitations merit particular attention. As far as data protection is concerned, the originating and selling bank's legitimate interest (e.g. to achieve regulatory capital relief by assigning loan receivables) should prevail over the interests of the debtor, especially with respect to non-performing loan receivables. In an NPE context bank secrecy should not be a material obstacle to disclosing information about the receivables. However, any disclosure should be made only at/after completion of the assignment of the receivables. Prior to completion, only loan balances (by law, loan balances are not subject to bank secrecy) and anonymised data should be disclosed.

From a regulatory perspective, the acquisition of loan receivables "on a commercial basis" may be performed only by credit institutions (local or EU/EEA under EU passporting rules) or by Bulgarian or EU/EFA financial institutions registered with the Bulgarian National Bank. While the latter registration does not imply fully fledged supervision (compared to a credit institution), it imposes certain minimum standards on the acquirer (e.g. minimum amount of capital, fit and proper requirements for the management or, in the case of an EU/EEA financial institution, registration with a national regulator).

Loan receivables (whether performing or not) and related security interests can be transferred either by assignment or, likely, by contractual subrogation (in any case, a notification of the debtor would be required). Assignments need to be registered to be effective with respect to certain types of security interests (notably real estate mortgages and non-possessory pledges) and, depending on portfolio size, such registrations may be time-consuming and costly. Contractual subrogation, which was not, to our knowledge, tested before Bulgarian courts, is supported by legal scholars and would not require any registration.

croatia

NPE transactions are often structured as an assignment (asset deal) in Croatia; however, share deals have also been seen in practice. NPE assignment documentation will have to comply with the requirements imposed by the Croatian National Bank. Also, in case a Croatian bank sells a "material amount of placements", the NPE assignment documentation will have to be approved in advance by the Croatian National Bank.

To the extent the assignment of an NPE involves secured loan receivables, the transfer of related security (mortgages, pledges, fiduciary assignments, etc.) will be, in general, perfected only upon re-registration with the competent public registers.

As regards bank secrecy obligations, banks are by law relieved from confidentiality to the extent necessary to conclude and perform transfers of receivables (to a regulated or non-regulated entity). This statutory secrecy exemption usually also applies at due diligence stages; however, it is recommended to conduct a prior assessment of this aspect before each transaction.

When it comes to servicing the purchased NPEs, pending court procedures will have to be carefully considered. For example, the buyer stepping into active litigation may be critical, since in certain instances this could require the debtor's consent. As to enforcement proceedings, the situation may vary depending on whether the enforcement is conducted under the pre-2014 or post-2014 enforcement rules.

czech republic

As far as banking secrecy is concerned, Czech Supreme Court decisions support the view that banking secrecy obligations do not prevent a credit institution from assigning its receivables. Similarly, data protection legislation limiting disclosure of data must be considered, especially when consumer credit portfolios are being handled. As the Czech Office for Personal Data Protection is known for its strict enforcement practice, anonymising customer information for due diligence purposes is highly recommended.

NPE transactions usually take the form of an assignment of receivables (an asset deal). While notification is not a requirement for the validity of the assignment, until the debtor is notified, it may successfully discharge the assigned receivables to the assignor.

The change of creditor also must be notified to the parties granting the security (until notified, no effects of the assignment arise towards them) and to the respective registry if the security is registered in the public registers. Such notification, however, does not constitute a re-registration and security interests can therefore be enforced by the assignee based on an assignment agreement without additional perfection or re-registration steps required.

The acquisition of NPE portfolios is not regarded as a regulated activity. Servicing and collection, however, require a local trade licence.

hungary

The major hurdle of operating on the Hungarian market is the licensing requirement. Purchasing of loan receivables, even if non-performing, requires a banking licence. While passporting is also theoretically available for EU-based investors, establishment is generally required in Hungary if Hungarian NPEs are purchased and serviced.

Banking secrecy regulation is favourable to the prospective purchasers. Pursuant to the guideline of the Hungarian National Bank, the data (even client's data) necessary for the purchase may be transferred to a prospective purchaser in the course of due diligence. Thus, there is no need for structured data rooms and complicated data transfers in the due diligence and negotiation phases.

Nevertheless, data subject to banking secrecy and data protection can only be transferred when enforcing the loan receivables if this is in the best interest of the credit institution. From a deal structuring perspective, this mainly means that the purchaser services the portfolio itself, which is rather common on the Hungarian market.

Apart from maximum amount mortgages created before 15 March 2014, collateral, as a rule, transfers together with the secured receivable. Nevertheless, it is common market practice that the security is re-registered to the purchaser.

Although not market practice, the parties may elect to transfer the entire contractual position to the purchaser (as opposed to a standard assignment of receivables). This transfer of contract would require the consent of each individual debtor. However, the parties may turn to the Hungarian National Bank and obtain its approval to the transaction, which substitutes the consent of each debtor.

montenegro

In 2017, the Parliament of Montenegro enacted the Law on Financial Leasing, Factoring, Purchase of Receivables, Micro-Lending and Credit-Guarantee Operations (the "Law").

The Law introduced, among other things, a distinction between factoring and purchase of receivables. Thus, depending on the type of receivables, factoring and purchase of receivables transactions can be used in the context of NPEs, but under different legal regimes.

Both factoring and the purchase of receivables (when performed as commercial activities) are in principle reserved for regulated entities, i.e. factoring companies, or companies for the purchase of receivables, which are licensed by the Central Bank of Montenegro ("CBM") or Montenegrin banks with a special approval from the CBM.

Purchasers are also obliged to submit data to the credit register of the CBM and have a reporting obligation towards the CBM. Furthermore, banks planning to sell or purchase receivables worth more than EUR 50,000 are required to obtain a CBM opinion confirming that the sale/purchase is justified. In order to issue the above opinion, the sale/purchase agreement and information on how the price was determined must be submitted to the CBM.

The relevant authorities have yet to sufficiently clarify data protection and banking secrecy rules in the context of NPE transfers. The Law on Credit Institutions does, however, envisage that the disclosure of data in aggregate form in such a manner that individual or business data on the client cannot be identified does not represent disclosure of a banking secret.

Absent a non-assignment clause, receivables can be assigned, but the assignor is bound to notify the assigned debtor of the assignment. The transfer of related security (mortgages, pledges, etc.) will be perfected only upon re-registration with the competent registers.

north macedonia

NPE transactions have not been common in North Macedonia. Historically, Macedonian banks have rarely opted for disposals as means of resolving NPEs, preferring instead to enforce NPEs.

Nevertheless, non-residents (i.e. non-Macedonian entities) may legally acquire NPEs, but such transactions must be notified to the National Bank of North Macedonia.

Special attention must be given to banking secrecy rules. The letter of the law does not provide for clear exemption/application criteria with respect to NPEs and no regulatory or court guidance is available in this respect. Proactive safety measures will be advisable in practice.

Generally, NPEs governed by Macedonian law may be transferred from banks to any third party by way of assignment. Additional perfection requirements will be required (e.g. appropriate re-registrations with the competent security registers).

poland

NPE transactions are facilitated in Poland by enabling banks to freely trade in distressed receivables without the debtor's consent and relieving them from banking secrecy obligations, along with a favourable regulatory regime that does not subject purchasers to financial services licensing requirements.

In terms of structuring, sale to a special type of closed-end investment fund called a "securitisation fund" seems to be the most popular and advantageous structure for NPE portfolio transactions on the Polish market. Fund managers usually entrust servicing of receivables purchased, including debt collection, to special servicing companies, which require authorisation from the Polish Financial Supervision Authority.

Polish law further allows trades in receivables without the debtor's consent in case of so-called "lost receivables" (i.e. mainly receivables overdue for more than 12 months or receivables where the bank has initiated enforcement proceedings) as well as in a procedure referred to as "public sale of bank receivables". These two possibilities may have less practical significance, though, because of the tax benefits available to banks when selling portfolios to securitisation funds.

Banking secrecy regulations follow the above transaction mechanisms. While the secrecy exemption does not yet apply at the due diligence stage, this could be structured in a way that the bank mandates/endorses "clean-team" advisors.

The time-consuming and relatively costly transfer of receivables secured by mortgages or registered pledges is clearly the main difficulty for true sale transactions in secured Polish NPEs. As an alternative, Polish law provides for bankruptcy remote synthetic transfers (sub-participations).

Due to developments in regulations and case law concerning receivables which may be challenged by consumers (e.g. under loan/credit agreements denominated in currencies other than PLN), the relevant risk of challenge and unsuccessful enforcement of the receivable should be addressed in the documentation.

romania

Once the adverse tax regime that was introduced in 2017/2018 will be put aside (likely in 2021), we expect several (larger) sale projects may quickly come to market. In addition to tax aspects, regulatory, disclosure, consumer protection and true sale considerations still warrant particular attention.

The acquisition of (not accelerated) loan receivables is in principle reserved to regulated entities, either licensed locally or passported. Licensing requirements are more relaxed, however, with respect to (i) corporate NPEs, and (ii) "non-performing" consumer loans (i.e. DPD in excess of 90 days and whose repayment was accelerated by the lender or is already in enforcement proceedings). Conversely, certain mortgage (consumer) loans, even if they qualify as "non-performing", may only be acquired by licensed credit institutions.

Unlicensed purchasers of consumer loan receivables must be registered with the Romanian consumer protection authority (mostly an administrative registration and subject to periodic reporting obligations). Foreign acquisition vehicles will also be required to have at least a representative appointed in Romania. To our knowledge, assignments to securitisation vehicles have not been used to date in Romania.

Servicing consumer loans is a licensed activity since 1 January 2017, subject to supervision and sanctioning by the Romanian consumer protection authority. Servicing corporate loans is not yet regulated.

Romanian law does not contain an express exemption from data protection and banking secrecy requirements in relation to NPE assignments. Past practice has relied heavily on the "legitimate interest" exemption. In both areas, careful due diligence of the applicable contractual provisions in the underlying loan documentation will be required.

For true sale, NPE acquisitions are traditionally structured as an assignment of (monetary) loan receivables. The assignment of an NPEs portfolio must be registered in the National Registry for Movables Publicity. In addition, the registrations of security interests will have to be amended to reflect the assignment as well. Amendments in the Land Book registrations require that the assignment agreement concerning the underlying receivables be concluded in the form of an authentic deed in front of a Romanian public notary, subject to payment of certain ad valorem fees (up to 3 % of the face value of the assigned receivables).

serbia

Serbia still has an inflexible foreign exchange regime that prohibits cross-border sales and assignments of loan receivables. As such, a local acquisition company needs to be set up to acquire local customer receivables.

The sale of banking NPEs is subject to strict banking regulations. Serbian banking rules regulate in detail the assignment of banks' loan claims and receivables from clients. A Serbian bank may assign its Retail Loans to another bank only. There are no exceptions to this rule. Corporate Loans may exceptionally be sold and transferred to a non-bank (non-licensed entity) if those are bad-performing assets, i.e. (A) if such loans are past due (NPEs); or (B) if the loans are not yet past due, but (i) they are qualified as problematic, and (ii) they were classified as a problematic receivable on the most recent classification cut-off date preceding the assignment.

For true sale, receivables and ancillary rights are usually transferred by assignment. The re-registration of the ancillary security interests is recommended but is rarely done in practice. If the transaction relates to receivables deriving from foreign (cross-border) credit transactions, Serbian FX rules set out that the respective assignment agreement has to be concluded either as a tripartite agreement involving not only the originating lender and purchaser but also the debtor of the underlying receivable, or it is necessary to obtain consent to the assignment from the specific debtor, who in practice will have little to no incentive to become a party to such a transaction or to provide its consent.

The National Bank of Serbia has issued its guidance and regulator's interpretations of the rules on banking secrecy in the context of NPE sales in Serbia, aiming to facilitate the exchange of information. Under this guidance, all pre-signing efforts – notably the phases of due diligence review and negotiations – are interpreted as safe harbour exceptions from the strict rules of the banking secrecy regime. While this interpretation still needs to be confirmed by courts or made law, the existence of the regulator's guidance alone has significantly facilitated the NPE transactions.

slovakia

From a regulatory perspective, corporate NPE transactions are not considered a banking activity and the loans can generally be acquired by anyone. Since 2017, NPE transfers of housing and consumer loans is subject to a much stricter regime – these loans can be acquired only by banks, foreign banks, a branch of a foreign bank or creditors holding a special licence to provide consumer loans.

Pursuant to the Slovak Act on Banks, a bank may assign its loan receivable against clients and provide the assignee with the necessary documentation without the client's consent (bank secrecy exemption), but only if the debtor is, despite a written warning, in default for more than ninety (90) calendar days (again, stricter rules apply for housing and consumer loans). However, the law does not provide any exemption with respect to a potential due diligence by the buyer before the actual purchase, which therefore requires careful structuring. Adhering to these strict requirements – unless consents of clients were obtained – makes any due diligence exercise and the preparation of the documents for the review by the potential purchaser quite burdensome. Due to similar concerns, data protection laws must be considered.

In general, NPE transactions take the form of an assignment of receivables. Accessory rights (such as interest or default interest) as well as security instruments are automatically transferred by operation of law. Transfer of other related rights, if any, must be explicitly agreed.

Enforcement of claims involves Slovak courts and enforcement officers, except for enforcement of pledges, where a direct out-of-court sale or auction is also possible. Banks do not enjoy any enforcement privileges compared to other non-regulated private creditors.

slovenia

Since 2014, Slovenian banks have enthusiastically embraced disposal of non-performing exposures – portfolios and single tickets alike. The Slovenian NPE market has matured considerably since then.

Various legal transaction mechanisms have been tried and tested in practice. Debt can be transferred by means of (i) assignment (used most frequently), (ii) transfer of contract (very robust but requires debtor consent), (iii) synthetic (contractual) transfers, and (iv) demerger / spin-off by acquisition (typically used for complex portfolios). Difficult-to-transfer security often drives the choice of the mechanism. Structuring an effective transfer of the so-called "maximum mortgages" (a popular security interest with certain limitations on transferability) will typically be a matter of discussion.

Prospective purchasers (other than credit institutions) generally do not need a special licence to acquire corporate debt. In contrast, when acquiring retail exposures, purchasers need to be mindful of certain transferability restrictions attached to consumer debt. Some investors choose to establish locally licensed acquisition SPVs.

As in other jurisdictions, Slovenian banking secrecy and personal data protection rules need to be considered in deal structuring, particularly during the due diligence phase. Anonymised and selective (or staged) disclosure is often employed in this respect.

Customary post-closing deliverables include (i) notification of debtors (typically per-formed by the seller), and (ii) issuance of a notarised omnibus "confirmatory transfer deed" document, the purpose of which is to document the occurrence of transfer for use in various legal proceedings and to re-register security. The latter generally transfers automatically with the claim, but registers are nevertheless updated in this manner to ensure publicity effects. Post-closing steps also play a role in an attempted enforcement. Debtors sometimes employ a range of defences against the new creditor, including denying any business relationship with the new entity. Having the occurrence of the transaction properly documented helps to streamline the proceedings in these cases.

In terms of court enforcement mechanisms, banks generally do not enjoy special enforcement privileges. If no out-of-court enforcement has been agreed, secured claims will need to be enforced under regular enforcement procedures before Slovenian courts. To reduce time to collection, lenders often require that the loan agreements are entered into as a directly enforceable notarial deed.

türkiye

In the aftermath of its most severe banking and financial crisis in 2000 – 2001, Turkey has initiated an ambitious structural reform programme aimed at sanitising its banking and financial sector. As part of such structural renovation efforts, transactions in NPE portfolios have been introduced.

Asset management companies (AMC), defined in the Banking Law in 2005, are authorised entities that are permitted to engage in NPE transactions. Following the establishment of AMCs, financial institutions started consistently selling NPEs to AMCs. In 2019, the total amount of NPEs sold to AMCs reached TRY 9.3bln. A legislative change in 2017 is expected to further boost the NPE market, as the amendment paved the way to state-owned banks also being able to sell their NPE portfolios. State-owned banks currently represent more than 40 % of the domestic loan market; hence their entry into the NPE market (for which they have been rather hesitant in times of crisis) will considerably enlarge the supply-side of the equation.

Non-performing loan portfolios are transferred in the form of an assignment of receivables (asset transfer), for which the consent of the debtor is not required. Blanket assignments are not recognised, and the agreement providing for the assignment of receivables needs to set forth the specifics of each transferred receivable in the form prescribed by applicable legislation.

Turkish AMCs are recognised as important tax exemptions, including from value added taxes. However, exemptions applicable to transactions carried out by AMCs in respect to stamp tax and other banking and loan-related taxes (such as the local resource utilisation fund) are only available for a period of five years following the incorporation date of the corresponding AMC.

Contacts & Disclaimer

|

Schoenherr Vienna Martin Ebner

|

Schoenherr Bucharest Matei Florea Schoenherr Ljubljana Vid Kobe |

|

Austria Martin Ebner

Bosnia And Herzegovina / Montenegro / North Macedonia / Serbia Nikola Babić Vojimir Kurtic Petar Vucinic Jovan Barovic Andrea Lazarevska

Bulgaria Ilko Stoyanov Tsvetan Krumov

Croatia Ozren Kobsa

Czech Republic Ondrej Havlicek Matěj Šarapatka

|

Hungary Gergely Szaloki

Poland Pawel Halwa

Romania Matei Florea

Slovakia Schoenherr Bratislava Prievozská 4/A (Apollo II) SK-821 09 Bratislava Soňa Hekelová Alexandra Adamickova

Slovenia Vid Kobe

Turkey Levent Celepci

|

This guide has been prepared for information purposes only and does not purport to constitute (nor may it be interpreted as substituting) transaction-specific legal advice. It does not purport to be exhaustive in any respect.

This guide is based on the relevant laws and regulations as of 15 January 2021 and may therefore not present an accurate picture of the legal situation in the future.

Schoenherr accepts no liability, duty or responsibility whatsoever vis-à-vis you, any of your officers, directors or employees or any of your advisors or any other third party, with respect to the content of this guide or the conclusions drawn from its content.

All rights reserved.

Schönherr Rechtsanwälte GmbH Schottenring 19 | 1010 Vienna

T: +43 1 534 37 193 | M: +43 664 80060 3193 | E: m.ebner@schoenherr.eu

If you wish to discuss any of these issues in greater detail, please feel free to contact the authors of this guide or any of your usual contacts in our firm.

Authors: Martin Ebner / Matei Florea / Vid Kobe

You can download the guide here or read on below.

[Open the chapters by clicking on the respective chapter title. For chapter 3, you can pick and choose the countries you want to see answers for via the country bubbles above.]